Prominent short-seller Jim Chanos is probably one of the last true “bad news bears” you will find on Wall Street these days, save for Jim Grant and Nouriel Roubini.

Almost everywhere you turn, money managers still are bullish on U.S. equities going into 2014 even after the Standard & Poor’s 500’s 27 percent returns year-to-date and the Nasdaq is back to levels not seen since the height of the dot-com bubble in 1999.“We’re back to a glass half-full environment as opposed to a glass half-empty environment,” Chanos told Reuters during a wide ranging hour-long discussion two weeks ago. “If you’re the typical investor, it’s probably time to be a little bit more cautious.”Chanos, president and founder of Kynikos Associates, admittedly knows it has been a humbling year for his cohort, with some short only funds even closing up shop.But he told Reuters that the market is primed for short-sellers like him and as a result has gone out to raise capital for his mission: “Markets mean-revert and performance mean-reverts and even alpha mean-reverts if at least my last 30 years are any indication.

And the time to be doing this is when you feel like the village idiot and not an evil genius, to paraphrase my critics.”Chanos’ bearish views are so well respected that the New York Federal Reserve has even included him as one of the money managers on its investment advisory counsel.

By his own admission, Chanos said he tends to be the one most skeptical on the markets.Chanos knows bad news when he sees it as he is known as the man who almost single handedly vindicated short sellers by revealing the ongoing fraud at Enron and WorldCom. And he sounded the alarm bell early on struggling computer giant Hewlett Packard.

Just last week, he sent shares of CGI Group Inc., the parent of CGI Federal, which is the main contractor behind the U.S. government&rs! quo;s glitch-plagued HealthCare.gov website, under selling pressure after Newsweek revealed that Chanos had placed a major short position.Chanos spoke about his other shorts including Caterpillar and – yes, just in time for Christmas — coal stocks at the Reuters Global Investment Outlook Summit and even shared some of his observations on the 1 percent and what they owe the rest of us.

On the U.S. stock market Chanos: “A few years back, I felt the U.S. was the best house in a bad neighborhood for a cliché hackneyed term and certainly there were better places that I think on a macro basis to be short like China. Our thinking is changed on that now. I think that the U.S. market is pretty fully discounting an awful lot of good news. While one can never be precise on markets and that’s not why my clients pay me, we’re finding many more opportunities (on the short side) in the U.S markets than we found a few years ago. The U.S. market at roughly 1,800 on the S&P is trading at 19 times earnings. I am always sort of befuddled because people use a much lower figure on that…we went back and triple-checked trailing 12-month S&P 500 earnings and they are only $95. A lot of companies report earnings before the bad stuff and we’re talking about GAAP earnings – actually talking about real accounting earnings – they are only $95. So for you to believe that the market is only at 14 times, 15 times next year’s number, you have to make some pretty robust assumptions on earnings growth to get to $95 to that $120 or $125 figure.”Déjà vu all over again.

Continue reading: [blogs.reuters.com]

About the author:

Canadian Value

http://valueinvestorcanada.blogspot.com/

| Currently 4.80/512345 Rating: 4.8/5 (5 votes) |

Subscribe via Email

Subscribe RSS Comments

AlbertaSunwapta - 2 hours ago

I've noticing a lot more of the big mercedes SUVs rolling around our town.

further down the article... "Chanos: “At Sotheby’s basically it goes from 10 to 50 seemingly in every cycle since the late 80s. There are some reasons for that — contemporary art is what I call ‘socially acceptable conspicuous consumption.’ "

Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

SPY STOCK PRICE CHART

181.56 (1y: +28%) $(function() { var seriesOptions = [], yAxisOptions = [], name = 'SPY', display = ''; Highcharts.setOptions({ global: { useUTC: true } }); var d = new Date(); $current_day = d.getDay(); if ($current_day == 5 || $current_day == 0 || $current_day == 6){ day = 4; } else{ day = 7; } seriesOptions[0] = { id : name, animation:false, color: '#4572A7', lineWidth: 1, name : name.toUpperCase() + ' stock price', threshold : null, data : [[1356328800000,142.35],[1356501600000,141.75],[1356588000000,141.56],[1356674400000,140.03],[1356933600000,142.41],[1357106400000,146.06],[1357192800000,145.73],[1357279200000,146.37],[1357538400000,145.97],[1357624800000,145.55],[1357711200000,145.92],[1357797600000,147.08],[1357884000000,147.07],[1358143200000,146.97],[1358229600000,147.07],[1358316000000,147.05],[1358402400000,148],[1358488800000,148.33],[1358834400000,149.13],[1358920800000,149.37],[1359007200000,149.41],[1359093600000,150.25],[1359352800000,150.07],[1359439200000,150.66],[1359525600000,150.07],[1359612000000,149.7],[1359698400000,151.24],[1359957600000,149.53],[1360044000000,151.05],[1360130400000,151.16],[1360216800000,150.96],[1360303200000,151.8],[1360562400000,151.77],[1360648800000,152.02],[1360735200000,152.15],[1360821600000,152.29],[1360908000000,152.11],[1361253600000,153.25],[1361340000000,151.34],[1361426400000,150.42],[1361512800000,151.89],[1361772000000,149],[1361858400000,150.02],[1361944800000,151.91],[1362031200000,151.61],[1362117600000,152.11],[1362376800000,152.92],[1362463200000,154.29],[1362549600000,154.5],[1362636000000,154.78],[1362722400000,155.44],[1362978000000,156.03],[1363064400000,155.68],[1363150800000,155.91],[1363237200000,156.73],[1363323600000,155.83],[1363582800000,154.97],[1363669200000,154.61],[1363755600000,155.69],[1363842000000,154.36],[1363928400000,155.6],[1364187600000,154.95],[1364274000000,156.19],[1364360400000,156.19],[1364446800000,156.67],[1364533200000,156.67],[1364792400000,156.05],[1364878800000,156.82],[1364965200000,155.23],[1365051600000,155.86],[1365138000000,155.16],[1365397200000,156.21],[1365483600000,156.75],[1365570000000,158.67],[1365742800000,158.8],[1366002000000,155.12],[1366088400000,157.41],[1366174800000,155.11],[1366261200000,154.14],[1366347600000,155.48],[1366606800000,156.17],[1366693200000,157.78],[1366779600000,157.88],[1366866000000,158.52],[1366952400000,158.24],[1367211600000,159.3],[1367298000000,159.68],[1367384400000,158.28],[1367470800000,159.75]! ,[1367557200000,161.37],[1367816400000,161.78],[1367902800000,162.6],[1367989200000,163.34],[1368075600000,162.88],[1368162000000,163.41],[1368421200000,163.54],[1368507600000,165.23],[1368594000000,166.12],[1368680400000,165.34],[1368766800000,166.94],[1369026000000,166.93],[1369112400000,167.17],[1369198800000,165.93],[1369285200000,165.45],[1369371600000,165.31],[1369630800000,165.31],[1369717200000,166.3],[1369803600000,165.22],[1369890000000,165.83],[1369976400000,163.45],[1370235600000,164.35],[1370322000000,163.56],[1370408400000,161.27],[1370494800000,162.73],[1370581200000,164.8],[1370840400000,164.8

Courtesy: WWE ORLANDO, Fla. -- Bodies crashing to the ground and being slung against the springy ropes of the ring. The slapping of skin as hulking men and women grapple and hurl blows at one another. The clink of free weights and the roar of broadcasters practicing to get it just right for the cameras. Welcome to World Wrestling Entertainment's (WWE) Performance Center, a $2.5 million, 26,000-square foot facility that opened last month, replacing a much smaller and antiquated facility in Tampa. It's both a graduate school of sorts for the WWE's next generation of talent and a training and rehabilitation center for its top-tier pro wrestlers, called "Superstars" and "Divas." "Most kids grow up and at least at some point in their lives want to be a fireman or a cop. I've always wanted to be a pro wrestler since I was a little kid," said 29-year-old Corey Graves, one of the 75 aspiring wrestlers based at the center. The largest part of the facility is a vast space featuring seven wrestling rings that makes the new Orlando facility the largest training facility WWE has ever built. Wrestler Xavier Woods, 26, said it's the kind of environment he always hoped to train in. "When I first started, the guy that was training us rented out the back of a storage unit, just a tight little space with bugs and everything. It was like the lowest-level thing you could do," Woods said. "So to be in a place like this ... it's literally unreal." Aspiring wrestlers currently in training range from former NFL players and Olympians to a former beauty pageant contestant. They signed contracts allowing them to work solely on becoming wrestlers. "One hundred percent, this is their jobs," said Jane Geddes, WWE senior vice president of talent and development.

Courtesy: WWE ORLANDO, Fla. -- Bodies crashing to the ground and being slung against the springy ropes of the ring. The slapping of skin as hulking men and women grapple and hurl blows at one another. The clink of free weights and the roar of broadcasters practicing to get it just right for the cameras. Welcome to World Wrestling Entertainment's (WWE) Performance Center, a $2.5 million, 26,000-square foot facility that opened last month, replacing a much smaller and antiquated facility in Tampa. It's both a graduate school of sorts for the WWE's next generation of talent and a training and rehabilitation center for its top-tier pro wrestlers, called "Superstars" and "Divas." "Most kids grow up and at least at some point in their lives want to be a fireman or a cop. I've always wanted to be a pro wrestler since I was a little kid," said 29-year-old Corey Graves, one of the 75 aspiring wrestlers based at the center. The largest part of the facility is a vast space featuring seven wrestling rings that makes the new Orlando facility the largest training facility WWE has ever built. Wrestler Xavier Woods, 26, said it's the kind of environment he always hoped to train in. "When I first started, the guy that was training us rented out the back of a storage unit, just a tight little space with bugs and everything. It was like the lowest-level thing you could do," Woods said. "So to be in a place like this ... it's literally unreal." Aspiring wrestlers currently in training range from former NFL players and Olympians to a former beauty pageant contestant. They signed contracts allowing them to work solely on becoming wrestlers. "One hundred percent, this is their jobs," said Jane Geddes, WWE senior vice president of talent and development.  Courtesy: WWE Geddes said the WWE built the center envisioning a place where up-and-comers could train alongside established professionals. WWE is the major leagues of pro wrestling, with a half-billion dollars in annual revenue. Traditionally, it has been a magnet for young talent from smaller, independent wrestling operations. But those minor leagues are dwindling, and while the WWE does still hold some open tryouts, the performance center will be its main training ground for developing talent. "This is where it starts for professional wrestlers now and this is where it will end -- in a good way -- as they look to move up to our main roster," Geddes said. "The timing was perfect for us to be able to move to the next level and create a facility like this." Those who succeed will advance to WWE's "Raw" and "Smackdown" television broadcasts, as well as to pay-per-view shows, including "WrestleMania." In the meantime, they split training time with appearances in WWE's weekly "NXT" shows, which are filmed live in front of a crowd of 500 at nearby Full Sail University, a school with a heavy emphasis on entertainment production. The one-hour shows are broadcast in 100 countries. While the performance center is mainly occupied by its "NXT" talent going through training, one of WWE's biggest stars, Paul "Big Show" Wight, was there recently to rehab from hip surgery. WWE's old Tampa facility had only three wrestling rings and was located in a warehouse with no air conditioning. The new facility is triple the size. It has an area where television announcers hone their craft, a studio where wrestlers practice television promos, as well as lockers, weight rooms and rehabilitation facilities that are NFL and NBA caliber. In many ways, developing wrestling characters is just as important as physical skill, as big, over-the-top personas like Hulk Hogan and Dwayne "The Rock" Johnson are what sell the sport. Everything the wrestlers do at the facility, from their development in the ring and in front of the camera during promo sessions, can be sent electronically back to WWE headquarters in Stamford, Conn. There's no set period for how long a wrestler will spend at the performance center before moving up to the big time, but at the new training hub, wrestlers like Woods and Graves are confident they have what they need to succeed. "Everything is right at our fingertips," Graves said. "You can actually feel a part of the big machine, which is really cool, because it can get frustrating when you think you're on your own. But now it's like, you're in it."

Courtesy: WWE Geddes said the WWE built the center envisioning a place where up-and-comers could train alongside established professionals. WWE is the major leagues of pro wrestling, with a half-billion dollars in annual revenue. Traditionally, it has been a magnet for young talent from smaller, independent wrestling operations. But those minor leagues are dwindling, and while the WWE does still hold some open tryouts, the performance center will be its main training ground for developing talent. "This is where it starts for professional wrestlers now and this is where it will end -- in a good way -- as they look to move up to our main roster," Geddes said. "The timing was perfect for us to be able to move to the next level and create a facility like this." Those who succeed will advance to WWE's "Raw" and "Smackdown" television broadcasts, as well as to pay-per-view shows, including "WrestleMania." In the meantime, they split training time with appearances in WWE's weekly "NXT" shows, which are filmed live in front of a crowd of 500 at nearby Full Sail University, a school with a heavy emphasis on entertainment production. The one-hour shows are broadcast in 100 countries. While the performance center is mainly occupied by its "NXT" talent going through training, one of WWE's biggest stars, Paul "Big Show" Wight, was there recently to rehab from hip surgery. WWE's old Tampa facility had only three wrestling rings and was located in a warehouse with no air conditioning. The new facility is triple the size. It has an area where television announcers hone their craft, a studio where wrestlers practice television promos, as well as lockers, weight rooms and rehabilitation facilities that are NFL and NBA caliber. In many ways, developing wrestling characters is just as important as physical skill, as big, over-the-top personas like Hulk Hogan and Dwayne "The Rock" Johnson are what sell the sport. Everything the wrestlers do at the facility, from their development in the ring and in front of the camera during promo sessions, can be sent electronically back to WWE headquarters in Stamford, Conn. There's no set period for how long a wrestler will spend at the performance center before moving up to the big time, but at the new training hub, wrestlers like Woods and Graves are confident they have what they need to succeed. "Everything is right at our fingertips," Graves said. "You can actually feel a part of the big machine, which is really cool, because it can get frustrating when you think you're on your own. But now it's like, you're in it."

Target: No guns in our stores, please NEW YORK (CNNMoney) If you're heading to Target, leave your guns at home.

Target: No guns in our stores, please NEW YORK (CNNMoney) If you're heading to Target, leave your guns at home.

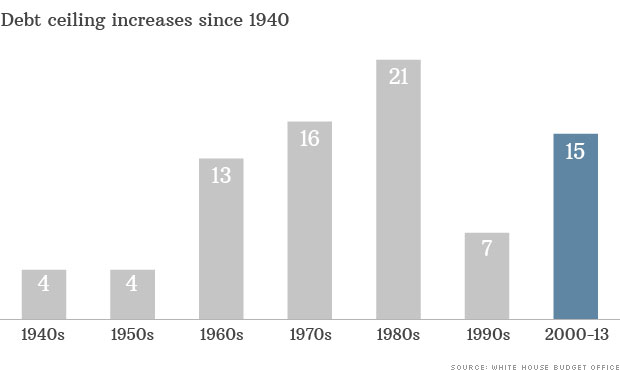

NEW YORK (CNNMoney) Here's how the latest episode of the debt ceiling drama will end: Congress will eventually raise or suspend the country's borrowing limit, probably for as much as a year.

NEW YORK (CNNMoney) Here's how the latest episode of the debt ceiling drama will end: Congress will eventually raise or suspend the country's borrowing limit, probably for as much as a year.

REUTERS

REUTERS