J.C. Penney's (NYSE: JCP ) stock fell more than 50% in the past 12 months and has increasingly underperformed the market for more than a decade. A few weeks ago, first-quarter earnings beat estimates and showed some signs of improvement. However, is J.C. Penney showing real improvement over other big-name rivals like Kohl's (NYSE: KSS ) and Target (NYSE: TGT ) ? Or was J.C. Penney's recent quarter just a fluke?

By Mike Kalasnik, via Wikimedia Commons

Viewing J.C. Penney's earnings against its peers

J.C. Penney's revenue was up 6.3% to $2.8 billion in its first quarter. Net income, however, fell 1.1% to a loss of $352 million. The two big metrics that impressed the market, though, were that same-store sales were up 6.2% and overall earnings per share came in better than what analysts expected.

In contrast to J.C. Penney, Kohl's quarter was a lot worse overall. Net income plunged 15% to $125 million on sales that fell 3.1% to $4.1 billion. Earnings per share fell 9%, while same-store sales worsened from the 1.9% decline a year ago to a drop of 3.4%.

Even though Target saw its revenue rise 2.1% to $17.1 billion, net income fell 16% to $418 million. The company is still recovering from the data breach, as store traffic dropped 2.3% in the quarter.

The market has pushed J.C. Penney shares past both Kohl's and Target; this is not only based on its recent quarter but on the hope that the turnaround is just in the beginning stages and that the shares have significant upside potential.

Are Kohl's days of paradise over? By MattL90, via Wikimedia Commons

The perfect storm for J.C. Penney?

There is significant evidence suggesting that J.C. Penney's recent rise is the byproduct of a competitor's recent struggles.

Kohl's was once a name synonymous with growth among retailers. From 1994-2004, the stock saw more than 700% in gains. In the past 10 years, the stock has produced slightly more than 31% in returns, not including dividends.

In its conference call, Kohl's blamed the weather for its e-commerce issues due to the ship-from-store system only being in place in 200 stores currently. However, a bigger issue may exist in the overall business model.

Kohl's is known for its predictable monthly sales and Kohl's Cash program that rewards customers when purchases exceed certain minimums. Customers are likely putting off purchases until the monthly sale rolls around to make bigger purchases at once in order to also receive Kohl's Cash. This would explain the decline in store traffic and the big drop in net income, which was likely affected by items being sold at promotional prices.

Target is facing its own issues that grew out of the data breach that occurred at year-end 2013. Ongoing costs and future costs to support higher security measures will weigh down the company for several quarters.

Target's Canadian segment continues to underperform, and the company is undergoing new leadership changes that include a new CEO and a new Canadian head.

J.C. Penney's position in retail improves significantly when you consider the target customers of these three companies.

Both Kohl's and Target are in a tough position because they are both getting squeezed at the high and low ends of retail. Both have a problem attracting the middle-end consumer, who continues to evolve depending on the overall economy. As a result, targeting middle-income customers is a lot harder than offering the lowest prices or introducing products for luxury customers.

Lastly, bad weather may give J.C. Penney an edge. The majority of Kohl's and Target locations are positioned in outdoor shopping centers, and some of them operate as stand-alone stores. Half of the 1,050 indoor and open air malls in the U.S. have J.C. Penney as an anchor tenant. Because of this, J.C. Penney has had the advantage of more potential foot traffic due to customers visiting other stores at the mall.

Obstacles didn't disappear for J.C. Penney's

Store traffic for J.C. Penney was still negative this past quarter despite April being the first month of positive results in two-and-a-half years. J.C. Penney continues to close its stores. At the end of FY 2012, there were 1,104 stores. At the end of this past fiscal year, there were 1,094 stores. While this news isn't terrible, especially since the online business grew 25.7% last quarter, it goes against J.C. Penney's self-imposed long-term goal -- to increase foot traffic in stores. With more than 30 stores being closed this year, mostly in malls, J.C. Penney is slowly losing its brick-and-mortar presence.

Possibly J.C. Penney's biggest obstacle: empty malls. By Jtalledo, via Wikimedia Commons

The fact that large indoor malls are quickly becoming obsolete may be the biggest burden of all for J.C. Penney over the long-term. Only six new indoor malls have been built in the U.S since 2010, a far cry from indoor mall growth during the 1980's.

Bottom line

J.C. Penney still has raised doubts among many investors. The company's stock has a large short interest of more than 30%. As a result, stock price pops on good news may be partly due to short covering.

J.C. Penney still needs to find a strategy to differentiate itself from its peers that goes beyond Kohl's and Target. Customers need to know what J.C. Penney brings to the table that others don't. While growing same-stores sales is indeed a positive, it doesn't mean much when many of these sales are at promotional or clearance prices.

Leaked: Apple's next smart device (warning, it may shock you)

Apple recent recruited a secret-development "dream team" to guarantee their newest smart device was kept hidden from the public for as long as possible. But the secret is out, and some early viewers are even claiming its everyday impact could trump the iPod, iPhone, and the iPad. In fact, ABI Research predicts 485 million of these type of devices will be sold per year. But one small company makes this gadget possible. And their stock price has nearly unlimited room to run for early in-the-know investors. To be one of them, and see Apple's newest smart gizmo, just click here!

Popular Posts: Buy These 3 Cheap Stocks Before It's Too Late3 ‘Forever Hold’ Stocks, 3 Ways to Make Income4 Reasons to Buy Disney Stock NOW Recent Posts: 3 Unknown Dividend Stocks to Buy Now Trading Gold? Try Options on GLD and GDX Want Stability? Try 200 Years of Growth View All Posts

Popular Posts: Buy These 3 Cheap Stocks Before It's Too Late3 ‘Forever Hold’ Stocks, 3 Ways to Make Income4 Reasons to Buy Disney Stock NOW Recent Posts: 3 Unknown Dividend Stocks to Buy Now Trading Gold? Try Options on GLD and GDX Want Stability? Try 200 Years of Growth View All Posts  Another thing to look for is how long a stock has been paying its dividend. Companies that have been throwing cash back at shareholders for a long time are likely to continue doing so, and these are the dividend stocks to pay attention to. The more obscure ones, usually with boring names, are another place to look because they may be underfollowed, and possibly undervalued.

Another thing to look for is how long a stock has been paying its dividend. Companies that have been throwing cash back at shareholders for a long time are likely to continue doing so, and these are the dividend stocks to pay attention to. The more obscure ones, usually with boring names, are another place to look because they may be underfollowed, and possibly undervalued. Dividend yield: 4.4%

Dividend yield: 4.4% Dividend yield: 3.7%

Dividend yield: 3.7% Dividend yield: 3.9%

Dividend yield: 3.9%

MORE GURUFOCUS LINKS

MORE GURUFOCUS LINKS  191.44 (1y: +16%) $(function(){var seriesOptions=[],yAxisOptions=[],name='SPY',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1369803600000,165.22],[1369890000000,165.83],[1369976400000,163.45],[1370235600000,164.35],[1370322000000,163.56],[1370408400000,161.27],[1370494800000,162.73],[1370581200000,164.8],[1370840400000,164.8],[1370926800000,163.1],[1371013200000,161.75],[1371099600000,164.21],[1371186000000,163.18],[1371358800000,163.18],[1371445200000,164.44],[1371531600000,165.74],[1371618000000,163.45],[1371704400000,159.4],[1371790800000,159.07],[1372050000000,157.06],[1372136400000,158.58],[1372222800000,160.14],[1372309200000,161.08],[1372395600000,160.42],[1372654800000,161.36],[1372741200000,161.21],[1372827600000,161.28],[1372914000000,161.28],[1373000400000,163.02],[1373259600000,163.95],[1373346000000,165.13],[1373432400000,165.19],[1373518800000,167.44],[1373605200000,167.51],[1373864400000,168.16],[1373950800000,167.53],[1374037200000,167.95],[1374123600000,168.87],[1374210000000,169.17],[1374469200000,169.5],[1374555600000,169.14],[1374642000000,168.52],[1374728400000,168.93],[1374814800000,169.11],[1375074000000,168.59],[1375160400000,168.59],[1375246800000,168.71],[1375333200000,170.66],[1375419600000,170.95],[1375678800000,170.7],[1375765200000,169.73],[1375851600000,169.18],[1375938000000,169.8],[1376024400000,169.31],[1376283600000,169.11],[1376370000000,169.61],[1376456400000,168.74],[1376542800000,166.38],[1376629200000,165.83],[1376888400000,164.77],[1376974800000,165.58],[1377061200000,164.56],[1377147600000,166.06],[1377234000000,166.62],[1377493200000,166],[1377579600000,163.33],[1377666000000,163.91],[1377752400000,164.17],[1377838800000,163.65],[1378098000000,163.65],[1378184400000,164.39],[1378270800000,165.75],[1378357200000,165.96],[1378443600000,166.04],[1378702800000,167.63],[1378789200000,168.87],[1378875600000,169.4],[1378962000000,168.95],[1379048400000,169.33],[1379307600000,170.31],[1379394000000,171.07],[1379480400000,173.05],[1379566800000,172.76],[1379653200! 000,170.72],[1379912400000,169.93],[1379998800000,169.53],[1380085200000,169.04],[1380171600000,169.69],[1380258000000,168.91],[1380517200000,168.01],[1380603600000,169.34],[1380690000000,169.18],[1380776400000,167.62],[1380862800000,168.89],[1381122000000,167.43],[1381208400000,165.48],[1381294800000,165.6],[1381381200000,169.17],[1381467600000,170.26],[1381726800000,170.94],[1381813200000,169.7],[1381899600000,172.07],[1381986000000,173.22],[1382072400000,174.39],[1382331600000,174.4],[1382418000000,175.41],[1382504400000,174.57],[1382590800000,175.15],[1382677200000,175.95],[1382936400000,176.23],[1383022800000,177.17],[1383109200000,176.29],[1383195600000,175.79],[1383282000000,176.21],[1383544800000,176.83],[1383631200000,176.27],[1383717600000,177.17],[1383804000000,174.93],[1383890400000,177.29],[1384149600000,177.32],[1384236000000,176.96],[1384322400000,178.38],[1384408800000,179.27],[1384495200000,180.05],[1384754400000,179.42],[1384840800000,179.03],[1384927200000,178.47],[1385013600000,179.91],[1385100000000,180.81],[1385359200000,180.63],[1385445600000,180.68],[1385532000000,181.12],[1385618400000,181.12],[1385704800000,181],[1385964000000,180.53],[1386050400000,179.75],[1386136800000,179.73],[1386223200000,178.94],[1386309600000,180.94],[1386568800000,181.4],[1386655200000,180.75],[1386741600000,178.72],[1386828000000,178.13],[1386914400000,178.11],[1387173600000,179.22],[1387260000000,178.65],[1387346400000,181.7],[1387432800000,181.49],[1387519200000,181.56],[1387778400000,182.53],[1387864800000,182.93],[1387951200000,182.93],[1388037600000,183.86],[1388124000000,183.85],[1388383200000,183.82],[1388469600000,184.69],[1388556000000,184.69],[1388642400000,182.92],[1388728800000,182.89],[1388988000000,182.36],[1389074400000,183.48],[1389160800000,183.52],[1389247200000,183.64],[1389333600000,184.14],[1389592800000,181.69],[1389679200000,183.67],[1389765600000,184.66],[1389852000000,184.42],[1389938400000,183.64],[1390197600000,183.64],[1390284000000,184.18],[1390370400000,184.3],[1390456800! 000,182.7! 9],[1390543200000,178.89],[1390802400000,178.01],[1390888800000,179.07],[1390975200000,177.35],[1391061600000,179.23],[1391148000000,178.18],[1391407200000,174.17],[1391493600000,175.39],[1391580000000,175.17],[1391666400000,177.48],[1391752800000,179.68],[1392012000000,180.01],[1392098400000,181.98],[1392184800000,182.07],[1392271200000,183.01],[1392357600000,184.02],[1392616800000,184.02],[1392703200000,184.24],[1392789600000,183.02],[1392876000000,184.1],[1392962400000,183.89],[1393221600000,184.91],[1393308000000,184.84],[1393394400000,184.85],[1393480800000,185.82],[1393567200000,

191.44 (1y: +16%) $(function(){var seriesOptions=[],yAxisOptions=[],name='SPY',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1369803600000,165.22],[1369890000000,165.83],[1369976400000,163.45],[1370235600000,164.35],[1370322000000,163.56],[1370408400000,161.27],[1370494800000,162.73],[1370581200000,164.8],[1370840400000,164.8],[1370926800000,163.1],[1371013200000,161.75],[1371099600000,164.21],[1371186000000,163.18],[1371358800000,163.18],[1371445200000,164.44],[1371531600000,165.74],[1371618000000,163.45],[1371704400000,159.4],[1371790800000,159.07],[1372050000000,157.06],[1372136400000,158.58],[1372222800000,160.14],[1372309200000,161.08],[1372395600000,160.42],[1372654800000,161.36],[1372741200000,161.21],[1372827600000,161.28],[1372914000000,161.28],[1373000400000,163.02],[1373259600000,163.95],[1373346000000,165.13],[1373432400000,165.19],[1373518800000,167.44],[1373605200000,167.51],[1373864400000,168.16],[1373950800000,167.53],[1374037200000,167.95],[1374123600000,168.87],[1374210000000,169.17],[1374469200000,169.5],[1374555600000,169.14],[1374642000000,168.52],[1374728400000,168.93],[1374814800000,169.11],[1375074000000,168.59],[1375160400000,168.59],[1375246800000,168.71],[1375333200000,170.66],[1375419600000,170.95],[1375678800000,170.7],[1375765200000,169.73],[1375851600000,169.18],[1375938000000,169.8],[1376024400000,169.31],[1376283600000,169.11],[1376370000000,169.61],[1376456400000,168.74],[1376542800000,166.38],[1376629200000,165.83],[1376888400000,164.77],[1376974800000,165.58],[1377061200000,164.56],[1377147600000,166.06],[1377234000000,166.62],[1377493200000,166],[1377579600000,163.33],[1377666000000,163.91],[1377752400000,164.17],[1377838800000,163.65],[1378098000000,163.65],[1378184400000,164.39],[1378270800000,165.75],[1378357200000,165.96],[1378443600000,166.04],[1378702800000,167.63],[1378789200000,168.87],[1378875600000,169.4],[1378962000000,168.95],[1379048400000,169.33],[1379307600000,170.31],[1379394000000,171.07],[1379480400000,173.05],[1379566800000,172.76],[1379653200! 000,170.72],[1379912400000,169.93],[1379998800000,169.53],[1380085200000,169.04],[1380171600000,169.69],[1380258000000,168.91],[1380517200000,168.01],[1380603600000,169.34],[1380690000000,169.18],[1380776400000,167.62],[1380862800000,168.89],[1381122000000,167.43],[1381208400000,165.48],[1381294800000,165.6],[1381381200000,169.17],[1381467600000,170.26],[1381726800000,170.94],[1381813200000,169.7],[1381899600000,172.07],[1381986000000,173.22],[1382072400000,174.39],[1382331600000,174.4],[1382418000000,175.41],[1382504400000,174.57],[1382590800000,175.15],[1382677200000,175.95],[1382936400000,176.23],[1383022800000,177.17],[1383109200000,176.29],[1383195600000,175.79],[1383282000000,176.21],[1383544800000,176.83],[1383631200000,176.27],[1383717600000,177.17],[1383804000000,174.93],[1383890400000,177.29],[1384149600000,177.32],[1384236000000,176.96],[1384322400000,178.38],[1384408800000,179.27],[1384495200000,180.05],[1384754400000,179.42],[1384840800000,179.03],[1384927200000,178.47],[1385013600000,179.91],[1385100000000,180.81],[1385359200000,180.63],[1385445600000,180.68],[1385532000000,181.12],[1385618400000,181.12],[1385704800000,181],[1385964000000,180.53],[1386050400000,179.75],[1386136800000,179.73],[1386223200000,178.94],[1386309600000,180.94],[1386568800000,181.4],[1386655200000,180.75],[1386741600000,178.72],[1386828000000,178.13],[1386914400000,178.11],[1387173600000,179.22],[1387260000000,178.65],[1387346400000,181.7],[1387432800000,181.49],[1387519200000,181.56],[1387778400000,182.53],[1387864800000,182.93],[1387951200000,182.93],[1388037600000,183.86],[1388124000000,183.85],[1388383200000,183.82],[1388469600000,184.69],[1388556000000,184.69],[1388642400000,182.92],[1388728800000,182.89],[1388988000000,182.36],[1389074400000,183.48],[1389160800000,183.52],[1389247200000,183.64],[1389333600000,184.14],[1389592800000,181.69],[1389679200000,183.67],[1389765600000,184.66],[1389852000000,184.42],[1389938400000,183.64],[1390197600000,183.64],[1390284000000,184.18],[1390370400000,184.3],[1390456800! 000,182.7! 9],[1390543200000,178.89],[1390802400000,178.01],[1390888800000,179.07],[1390975200000,177.35],[1391061600000,179.23],[1391148000000,178.18],[1391407200000,174.17],[1391493600000,175.39],[1391580000000,175.17],[1391666400000,177.48],[1391752800000,179.68],[1392012000000,180.01],[1392098400000,181.98],[1392184800000,182.07],[1392271200000,183.01],[1392357600000,184.02],[1392616800000,184.02],[1392703200000,184.24],[1392789600000,183.02],[1392876000000,184.1],[1392962400000,183.89],[1393221600000,184.91],[1393308000000,184.84],[1393394400000,184.85],[1393480800000,185.82],[1393567200000,

Getty Images

Getty Images  Getty Images

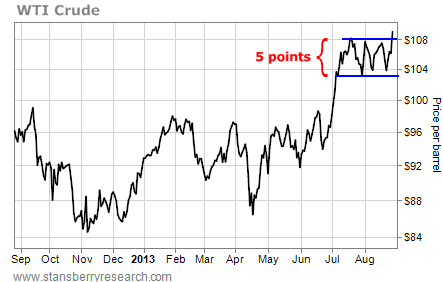

Getty Images  As you can see in the chart above, the difference between oil's recent support and resistance levels is about five points. So if we add five points to the breakout level of $108, we get a target price for oil of $113. That target price lines up well with the resistance of oil's former high price in 2011. Take a look at this longer-term chart...

As you can see in the chart above, the difference between oil's recent support and resistance levels is about five points. So if we add five points to the breakout level of $108, we get a target price for oil of $113. That target price lines up well with the resistance of oil's former high price in 2011. Take a look at this longer-term chart...  But there are still several reasons to be bearish on oil. Oil inventories are higher than average for this time of year and it has a seasonal tendency to decline in September. Also, demand for oil has been declining due to sluggish economic growth. The big reason to be bullish right now is the impending U.S. military action in Syria. That possibility trumps the supply/demand concerns. It has pushed oil to its highest price in two years. And it'll likely push prices a bit higher. But as the price of oil approaches the $113 target level and the threat of military action runs its course, oil is likely to form an important intermediate-term top. That will be the time for traders to take another shot at a short sale in the oil market. Best regards and good trading, Jeff Clark

But there are still several reasons to be bearish on oil. Oil inventories are higher than average for this time of year and it has a seasonal tendency to decline in September. Also, demand for oil has been declining due to sluggish economic growth. The big reason to be bullish right now is the impending U.S. military action in Syria. That possibility trumps the supply/demand concerns. It has pushed oil to its highest price in two years. And it'll likely push prices a bit higher. But as the price of oil approaches the $113 target level and the threat of military action runs its course, oil is likely to form an important intermediate-term top. That will be the time for traders to take another shot at a short sale in the oil market. Best regards and good trading, Jeff Clark